If you have power of attorney for an aging parent or loved one, you may assume that the document gives you the authority to handle their tax obligations, including filing their federal income tax return.

In practice, the IRS operates by its own rules, and navigating those rules requires IRS Form 2848, Power of Attorney and Declaration of Representative.

Understanding how this form works, who can use it, and how criminals are now exploiting it is essential knowledge for any family member or professional acting on behalf of a taxpayer.

What is IRS FORM 2848?

A power of attorney (POA) is a legal document that authorizes a designated individual, commonly called the “agent” or “attorney-in-fact”, to manage the affairs of another person, known as the “principal.”

POAs are used for a wide range of purposes: financial planning, medical decisions (in certain states), emergencies, or situations where someone is no longer able to manage their own affairs.

However, when it comes to IRS matters, a general POA is not enough. The IRS requires its own authorization document. Form 2848 is the primary instrument for authorizing an eligible individual to represent another person before the Internal Revenue Service.

Once accepted by the IRS, a properly filed Form 2848 enables the authorized representative to communicate with the IRS on the taxpayer’s behalf, receive confidential tax information, and perform certain acts – such as signing agreements or responding to IRS notices – within the scope of authority defined in the form.

Who Is Eligible to Be Named as a Representative?

Not everyone can be granted IRS power of attorney through Form 2848. The IRS limits representation rights to a specific class of qualified individuals:

Attorneys – members in good standing of the bar of the highest court in their jurisdiction

Certified Public Accountants (CPAs) – holders of an active CPA license

Enrolled Agents – federally authorized tax professionals enrolled by the IRS under the requirements of Circular 230

Enrolled Actuaries – enrolled under 29 U.S.C. 1242 (with limited scope of practice)

Immediate family members – including a spouse, parent, child, sibling, grandparent, or step-relative

Unenrolled return preparers – but only under limited circumstances, such as those who have completed the IRS Annual Filing Season Program and prepared the return in question

In all cases, representatives must supply their Preparer Tax Identification Number (PTIN) and, where applicable, their professional license number.

Completing and Filing Form 2848

The form consists of two main parts.

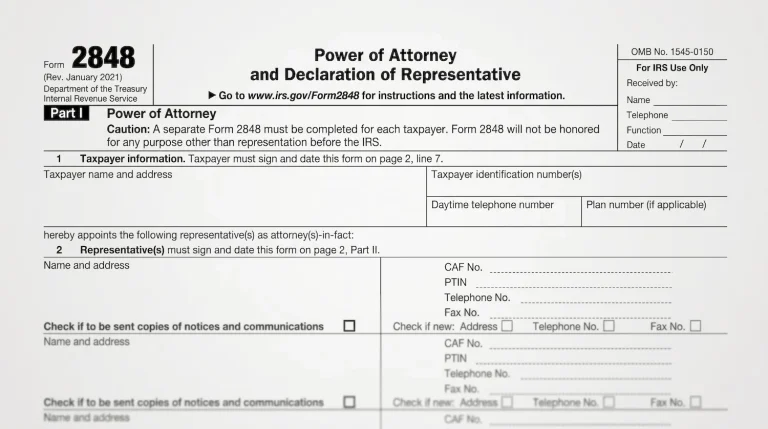

Part I of IRS Form 2848, Power of Attorney and Declaration of Representative, is used by a taxpayer to officially appoint one or more representatives to act on their behalf before the Internal Revenue Service. This section requires the disclosure of the taxpayer’s identifying information and the specific details of the designated representatives, including their Centralized Authorization File (CAF) and Preparer Tax Identification Numbers (PTIN).

Part II of Form 2848 requires the appointed representative to sign and date the document, declaring that they are authorized to represent the taxpayer and are aware of the regulations governing practice before the IRS. It also necessitates that the representative indicate their specific designation, such as an attorney, CPA, or enrolled agent, to verify their eligibility to act in this legal capacity.

Both the taxpayer and the representative must sign and date the form. If a joint return was filed for a relevant tax year, each spouse must complete a separate Form 2848 – even if they are appointing the same representative.

The form can be submitted online via the IRS’s Tax Pro Account portal, by fax to the appropriate Centralized Authorization File (CAF) unit, or by mail.

One important note: Form 2848 cannot be included electronically with a tax return. It is a separate submission.

Special Considerations for Aging Parents and Cognitively Impaired Individuals

Many adult children seek to use their power of attorney to file taxes on behalf of aging parents. This is one of the most common reasons families encounter Form 2848.

The requirement that both the principal and the representative must sign and date the form can pose a significant challenge when a parent suffers from cognitive decline, serious illness, or is otherwise unable to sign.

If the principal is infirm or out of the country, the representative may request the authority to sign the tax return on their behalf — but this requires specific IRS permission, and the reason for the principal’s inability to sign must be clearly documented and acknowledged by the IRS.

Planning ahead is key. If you anticipate needing to manage a loved one’s taxes in the future, it is far better to complete Form 2848 while the principal is still able to participate in the signing process. Waiting until cognitive decline becomes severe can create serious legal and logistical barriers.

For a broader look at how a financial power of attorney can intersect with elder financial exploitation, the Consumer Financial Protection Bureau has published a statement on recognizing and preventing such exploitation that is worth reviewing.

Scammers Are Now Exploiting Form 2848

An alarming development around Form 2848 is its misuse by fraudsters.

Scammers have discovered that this document, whether forged or obtained through deception, gives them access to a taxpayer’s confidential IRS records, which they can then exploit for identity theft or to redirect tax refunds.

- File fraudulent tax returns in the victim’s name

- Redirect tax refunds to accounts they control

- Access years of confidential financial records

What to Do If You Suspect Unauthorized Form 2848 Activity

If you discover or suspect that a fraudulent Form 2848 has been filed in your name – or on behalf of a loved one – it’s critical to act quickly. The IRS recommends the following steps:

Revoke the unauthorized POA immediately

The principal, if he or she has capacity, should submit a new Form 2848 or a written statement to the IRS Centralized Authorization File (CAF) unit with the word “Revoke“ written across it.

Obtain an Identity Protection (IP) PIN

This six-digit number prevents anyone else from filing a federal tax return using your Social Security number. The IRS Taxpayer Advocate has published a helpful guide on how to sign up for an IP PIN through your IRS Online Account.

Monitor your IRS Online Account

By creating an account at IRS.gov, taxpayers can view their tax balance, payment history, up to 5 years of tax records, and recent notices – including any filings of unauthorized POAs or representatives.

Monitoring your account regularly is one of the simplest and most effective ways to catch unauthorized activity early.

How EverSafe Can Help You Stay Protected

At EverSafe, we understand that protecting your financial identity goes far beyond watching your bank account. Tax-related identity theft, unauthorized POA filings, and IRS impersonation scams are among the fastest-growing threats facing older Americans and their families.

Our platform is designed to detect suspicious patterns — unusual account activity, unexpected changes to financial records, and signs that something may be wrong — and alert you or a trusted family member before damage spreads.

You can also monitor your IRS account online by creating or signing in at IRS.gov, where the agency’s secure tools allow you to view recent notices and confirm whether any representatives have been authorized on your behalf.

If you have questions about protecting yourself or a loved one from financial fraud, the EverSafe team is here to help. Learn more about how our monitoring service works.

This post is provided for general informational purposes only and does not constitute legal or tax advice. Please consult a qualified tax professional or attorney regarding your specific situation.

Liz Loewy, COO

Liz Loewy is the co-founder and Chief Operating Officer at EverSafe. A graduate of the University of Pennsylvania and Albany Law School, Liz was previously a prosecutor in the Manhattan District Attorney’s Office, where she oversaw the Office’s Domestic Violence Unit before founding its first Elder Abuse Unit – serving as its Chief for 18 years. Liz presented at the last White House Conference on Aging and has served as an expert witness as well as trial counsel on a number of criminal and civil cases involving financial fraud, including the successful prosecution involving the late Brooke Astor, who was exploited by her only son and his attorney. She has presented on the subject of elder financial abuse at conferences in the US and Europe and authored a number of publications, including a book entitled “Financial Exploitation of the Elderly: Legal Issues, Prevention, Prosecution, Social Service Advocacy” (Civic Research Institute).