Most people have heard of the big three credit bureaus – TransUnion, Equifax, and Experian – but few understand how differently they operate behind the scenes. Those differences matter more than you might think, especially when it comes to protecting yourself or an aging parent from fraud.

In this post, we’ll explain what credit monitoring actually does, compare the three major credit bureaus side by side, and make the case for why monitoring just one bureau is never enough.

What is Credit Monitoring?

At its core, credit monitoring alerts you to changes in your credit report. These changes can include new accounts opened in your name, hard credit inquiries, significant changes to your balance, and collection activity. Think of it as a notification system for your financial identity.

It’s a useful concept in theory. But the real value depends entirely on what data is being watched and how much of your credit file you can actually see. A monitoring service that tracks only a fraction of your credit activity can give you a false sense of security – and that gap is exactly what fraudsters exploit.

If you’ve ever been part of a data breach, you’ve probably received a familiar email offering “free credit monitoring.” It sounds reassuring, like someone has your back. But before you breathe easy, it’s worth understanding what that offer actually covers – and more importantly, what it doesn’t.

How the Big Three Credit Bureaus Collect Your Data

Each of the three major credit bureaus – Equifax, Experian, and TransUnion – independently gathers and maintains information about your credit history. They collect similar types of data: account balances, payment history, credit inquiries, public records like bankruptcies, and collection activity.

However, lenders and creditors are not required to report to all three bureaus. Some report to only one or two. That means your credit file at Equifax may contain accounts or activity that doesn’t appear in your files at TransUnion or Experian, and vice versa. Each bureau gets its information from different sources, which is why the information in one bureau’s report may not match the others.

This isn’t a flaw in the system – it’s simply how voluntary reporting works. But it creates real consequences for anyone relying on a single bureau for credit monitoring.

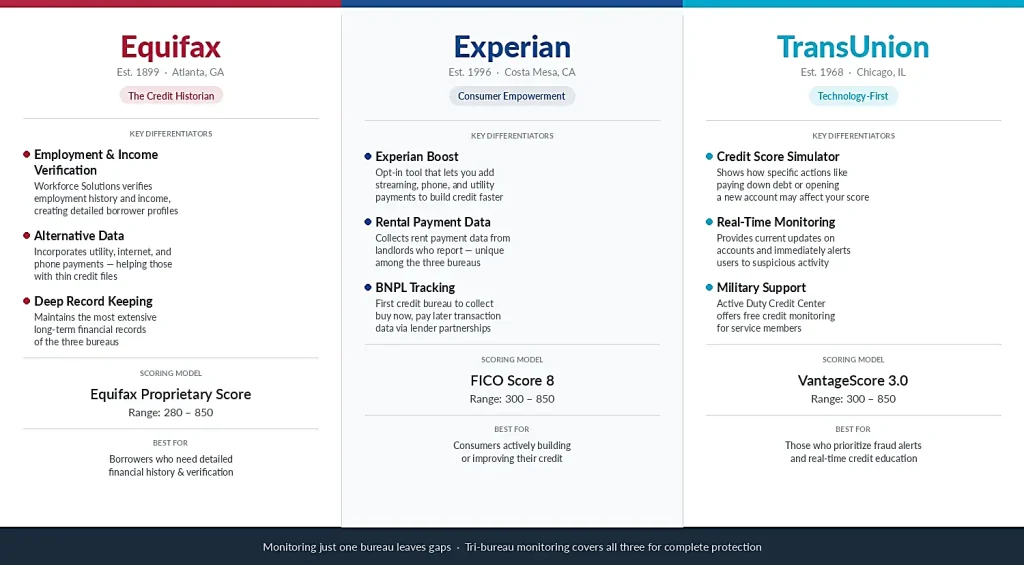

Equifax: The Credit Historian

Founded over 125 years ago, Equifax is the oldest of the big three credit bureaus. It’s known for maintaining deep, long-term financial records and for incorporating alternative data sources that the other bureaus may not capture.

Key characteristics of Equifax include:

- Employment and income verification: Equifax operates Workforce Solutions, a service that verifies employment history and income for businesses, adding an extra layer of detail to borrower profiles.

- Alternative data: Equifax incorporates data like utility, internet, and phone payments sourced directly from service providers. This helps individuals with thin credit files get recognized for paying their bills on time.

- Proprietary scoring tools: Equifax uses its own educational credit score, which ranges from 280 to 850, rather than relying solely on third-party models.

After a significant data breach in 2017 that exposed the personal information of approximately 147 million Americans, Equifax invested heavily in strengthening its data security and consumer transparency measures.

Experian: The Consumer Empowerment Bureau

Experian is the largest of the three bureaus by consumer coverage, maintaining credit information for over 220 million consumers in the United States. It’s distinguished by the tools it offers consumers to actively build and manage their own credit profiles.

What sets Experian apart:

- Experian Boost: This opt-in feature lets consumers add positive payment history from eligible accounts – such as streaming services, phone bills, and utilities – directly to their Experian credit file. Unlike Equifax’s behind-the-scenes alternative data, Experian Boost puts the consumer in control of what gets added.

- Rental payment data: Experian collects rental payment data from landlords who report it – information the other bureaus typically don’t capture.

- Buy Now, Pay Later tracking: Experian became the first credit bureau to collect “buy now, pay later” data through partnerships with services like Apple Pay Later.

- FICO Score 8: Experian uses the FICO Score 8 model, the most widely used scoring model among lenders, with a range of 300 to 850.

TransUnion: The Technology-First Bureau

TransUnion takes a technology-forward approach to credit reporting. It combines data science and analytics to help lenders make more informed decisions while also prioritizing consumer education and fraud prevention.

Notable features of TransUnion:

- Credit score simulator: TransUnion offers a tool that shows consumers how specific actions – such as paying down debt or opening a new account – could affect their credit score. This educational approach helps people understand their credit rather than just tracking it.

- Real-time monitoring: TransUnion works closely with lenders to provide up-to-date account information, and its identity protection and fraud monitoring services immediately alert users to suspicious activity.

- VantageScore 3.0: TransUnion uses the VantageScore 3.0 model for its consumer-facing credit scores, which range from 300 to 850. VantageScore was developed cooperatively by all three bureaus, meaning tri-bureau VantageScores using the same version will be identical for the same data.

- Military consumer support: TransUnion offers an Active Duty Credit Center with free credit monitoring for military consumers.

Why Your Credit Scores Differ Across Bureaus

If you’ve ever checked your credit score from more than one bureau, you likely noticed the numbers didn’t match. This isn’t an error – it reflects real differences in how each bureau operates.

There are three main reasons your scores vary:

Different data sources. Because creditor reporting is voluntary, each bureau’s credit file reflects a different subset of your financial activity. One bureau might show a collection account or a new credit line that the others don’t have.

Different scoring models. Equifax, Experian, and TransUnion each default to different scoring models for consumer-facing scores. The FICO Score 8, VantageScore 3.0, and Equifax’s proprietary model each weigh factors slightly differently. Even identical data can produce different results depending on the model.

Different update timing. Creditors don’t report to all bureaus on the same schedule. Your TransUnion file might reflect a recent payment, while your Experian file still shows the older balance.

In industries like mortgage lending, pulling data from all three bureaus has long been the gold standard precisely because more data means a more accurate picture. The same logic should apply to protecting yourself.

Why Single-Bureau Monitoring Leaves You Exposed

Many “free” monitoring offers – especially those provided after a data breach – cover only one bureau. This creates serious blind spots.

Here’s the problem: if a fraudster opens a credit card in your name and the issuing bank only reports to Experian, a monitoring service watching only your TransUnion file will never see it. You could go weeks, months, or even years without knowing about the fraud.

Identity theft is messy by design. Fraudulent activity often appears on one bureau first, then may or may not spread to the others. With single-bureau monitoring, you’re relying on the hope that the fraud happens to show up on the one bureau you’re watching.

That’s not protection – it’s a coin toss.

The risk is especially acute for older adults. According to the FTC, older adults reported losing far more money to fraud than younger consumers, and the losses for seniors over 60 who lost more than $100,000 increased eightfold between 2020 and 2024. For adult children monitoring a parent’s financial health, a single-bureau service can mean critical warning signs go undetected.

What Tri-Bureau Credit Monitoring Actually Covers

Tri-bureau monitoring – monitoring all three major credit bureaus – eliminates the blind spots that come with monitoring just one. It gives you a complete view of your credit activity across Equifax, Experian, and TransUnion simultaneously.

With tri-bureau monitoring, you can:

- Detect fraud faster. If a fraudulent account opens at any bureau, you’ll be alerted immediately rather than hoping it shows up on the one bureau you’re watching.

- See what lenders see. Because lenders can pull your credit from any of the three bureaus – and mortgage lenders typically pull from all three – tri-bureau monitoring gives you the same comprehensive view.

- Catch discrepancies. Errors on credit reports are more common than most people realize. Monitoring all three bureaus means you can spot and dispute inaccurate information wherever it appears.

- Get a more accurate financial picture. Your credit profile is not one report – it’s three separate files. Seeing all three is the only way to understand your full financial standing.

Incomplete protection is exactly what fraudsters count on. If your goal is to safeguard yourself or a loved one, monitoring a single bureau provides only partial visibility. Monitoring all three gives you significantly stronger protection.

Beyond the Big Three: Other Reporting Agencies

While Equifax, Experian, and TransUnion dominate the credit reporting landscape, they aren’t the only consumer reporting agencies. Specialty bureaus like Innovis, TeleTrack, and NCTUE also maintain consumer data, often focusing on specific types of accounts or populations.

In total, there are dozens of reporting bureaus, some national and some specialized. This is another reason comprehensive monitoring matters. The more of your financial activity you can see, the harder it is for fraud to hide in the gaps.

For those concerned about online security threats beyond credit fraud – such as account takeovers and phishing scams – layering credit monitoring with broader financial monitoring provides a more complete safety net.

How to Take Action and Protect Yourself

Understanding how the credit bureau system works is the first step. Here’s what you can do right now:

- Check your credit reports. You’re entitled to a free report from each bureau every year at AnnualCreditReport.com. The three bureaus currently offer free weekly reports as well.

- Freeze your credit. A credit freeze prevents new accounts from being opened in your name at each bureau. It’s free, doesn’t affect your score, and can be temporarily lifted when you need to apply for credit.

- Set up fraud alerts. A fraud alert tells lenders to verify your identity before extending new credit. You only need to set it with one bureau, and it will be shared with the other two.

Go Beyond Credit Monitoring

Credit monitoring alone won’t catch fraud involving bank accounts, investment accounts, or other financial activity that doesn’t appear on credit reports. Services that monitor across accounts and institutions provide a more comprehensive layer of defense. The FTC recommends taking a multi-layered approach to identity theft protection that goes beyond credit monitoring alone.

Whether you’re protecting your own financial identity or keeping an eye on an aging parent’s accounts, the key is visibility. The more you can see, the faster you can act. And as the AARP advises, routinely monitoring your credit report and financial accounts is one of the most effective steps you can take against fraud.

* * *

Your credit report isn’t one unified document. It’s three separate files maintained by three independent bureaus, each with different data sources, scoring models, and update schedules. Watching only one is like locking your front door but leaving the back door and windows wide open.

Single-bureau monitoring is cheaper, but it’s incomplete – and incomplete protection is exactly what fraudsters count on. If your goal is real protection for yourself or someone you love, tri-bureau credit monitoring isn’t overkill. It’s the only way to see the full picture.

It’s not about being paranoid. It’s about understanding how the system actually works – because when it comes to identity theft and fraud, what you don’t see can absolutely hurt you.

Howard Tischler, CEO

Howard is a veteran credit-industry executive with 25+ years of leadership experience across credit bureaus, loan decisioning technology, and consumer credit automation. He has served as CEO of First American CMSI, President of Teletrack, CEO of Credit Online (later merged with DealerTrack, where he was Lead Director for 15+ years), and is currently CEO of EverSafe. His career spans the full credit ecosystem – how credit data is created, analyzed, and deployed.